H

124

23 Pensions and other post-employment benefits (continued)

Ahold at a glance

Notes to the consolidated

financial statements

Our strategy

Our performance

Governan

Financials

Investors

Ahold Annual Report 2013

During 2013, Ahold changed the way it accounts for the contributions it makes to prepay disbursement costs that will be incurred when future benefits are paid to beneficiaries. These costs

were previously included in the defined benefit obligation of the pension plan for the Netherlands, but will now be expensed as contributions are made. This change has resulted in a reduction

of the 2013 year end defined benefit obligation of €102 million, which has been treated as a remeasurement and recognized within other comprehensive income.

During 2012, the Company amended its defined benefit pension plan in the Netherlands. The plan amendments included, among other changes, raising the retirement age and gradually

increasing the amount that participants will contribute in future years. The effect of all amendments was a net past service cost of €39 million.

During 2012, the Company changed its methodology for measuring past service years within the Dutch pension fund. The previous methodology was to calculate past service years based on

a participant's accrued benefits, but this has been changed to a methodology that uses the maximum past service years based on a participant's actual date of hire or accrued benefits. The

effect of the change on the 2012 year-end defined benefit obligation was an increase of €101 million, which was recognized as a remeasurement within other comprehensive income.

In 2008, the Company decided to transition its defined benefit pension plan for active salaried, non-union and certain union employees ("eligible employees") in the United States to a defined

contribution pension plan. Eligible employees who were at least 50 years of age or had 25 or more years of service as of December 312009, could choose to either stay in the defined benefit

plan or transfer to a 401(k) plan. All other eligible employees were transferred to a 401 (k) plan. Accrued benefits under the defined benefit plan for employees transferred to a 401 (k) plan were

frozen for pay and service as of December 31, 2009 (frozen plan). The resulting curtailment gain in 2008 was largely offset by accrued additional (transition) contributions that the Company

will make to a 401 (k) plan for a period of five years (201 0-2014) to employees meeting certain age or service requirements who were transferred to a 401(k) plan. During 2012, the Company

settled the frozen accrued benefits of participants who elected to receive a lump sum payout. At that time, the Company recognized a settlement gain of €6 million. In 201 3, the Company

settled the remaining frozen accrued benefits by purchasing annuity contracts, which resulted in a further settlement gain of €9 million.

Cash contributions

From 2013 to 2014, Company contributions are expected to decrease from €122 million to €114 million in the Netherlands and decrease from $81 million (€61 million) to $64 million (€47

million) in the United States.

As of year-end 2013, the funding ratio, calculated in accordance with regulatory requirements, of the largest Dutch plan was 116% and the U.S. pension plan was 112%. Under the financing

agreement with the Dutch pension fund, contributions are made as a percent of employees' salaries and shared between Ahold and the employees. The agreement also allows for a reduction

in premiums if certain funding conditions are met. In addition, Ahold can be required to contribute a maximum amount of €150 million over a five-year period if the funding ratio is below

105%. Contributions to the U.S. pension plan are required if the prior year-end funding ratio falls below 100% as measured under the Pension Protection Act.

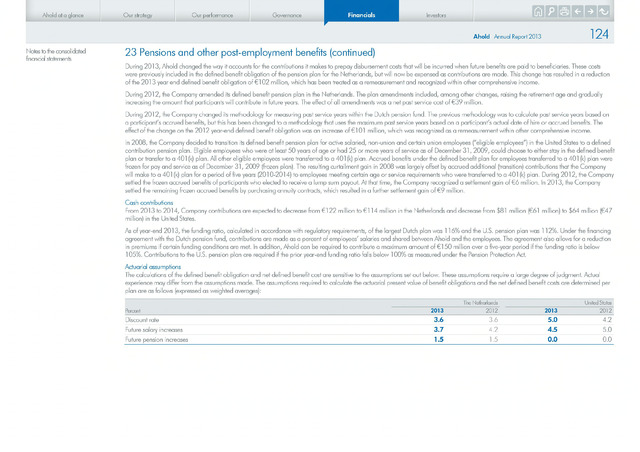

Actuarial assumptions

The calculations of the defined benefit obligation and net defined benefit cost are sensitive to the assumptions set out below. These assumptions require a large degree of judgment. Actual

experience may differ from the assumptions made. The assumptions required to calculate the actuarial present value of benefit obligations and the net defined benefit costs are determined per

plan are as follows (expressed as weighted averages):

Percent

2013

The Netherlands

2012

2013

United States

2012

Discount rate

3.6

3.6

5.0

4.2

Future salary increases

3.7

4.2

4.5

5.0

Future pension increases

1.5

1.5

0.0

0.0

{kind=link}